BOPP film has been one of the global success stories in flexible plastics packaging. This is now an industry which produces over 7 mln tpa of substrates, worth more than US$18 bln, according to a new report on the Global BOPP film market from AMI Consulting. However, it is increasingly an industry that is driven by markets and areas of the world that historically have been considered "developing nations". This is not just a function of market volumes and growth rates, but also market leadership as the major players in the BOPP market today are now head quartered in what AMI is calling the CHIME nations - China, India and the Middle East. Over the past three years the BOPP film industry has been through a period of major structural change with the emergence of two major power houses with sales in excess of US$ 1 bln: Jindal Poly Films based in India and Tahgleef Industries headquartered in Dubai. Jindal Poly Films takeover of ExxonMobil Chemical Films, completed in 2013, creates a group with the largest nameplate capacity for BOPP at over 400,000 tons with assets based in Europe, the USA as well as being the largest producer in India. Taghleef which AMI estimates to be just behind Jindal in capacity terms, has similarly built a global position through the acquisition of various heritage businesses in Europe and North America. In 2012 it completed the takeover of AET Films in the USA and only recently has announced another acquisition in Europe with the takeover of Derprosa in Spain. Despite these impressive moves, these two businesses still account for less than 10% of global production and are likely to be overtaken - on a volume basis at least - by Chinese producers over the next few years. The investment in capacity and growth in demand for BOPP films in China has been well documented but the leading producers there are now looking to move to whole different level. From the original business model of setting up a large plant with 3 or 4 big lines, the leading players are now looking to build a network of plants within China with state of the art 8.7 metre and 10.4 metre high speed (525 mts/minute and more) lines and to vertically integrate into polypropylene resin production. The rapid growth of businesses such as the Gettel Group and China Soft Packaging - backed by cash rich real estate businesses - is leading the Chinese industry to have its own structural shakeout. Many of the early movers there have sold off assets, moved out of the sector or are looking to develop more speciality, niche products unable to compete in the commodity packaging sector.

As per Global Industry Analysts, BOPP films represents one of the high-growth segments in the global plastic film & sheets industry. Over the near term, BOPP production capacity is estimated to expand by 2-3 million tons, with the Middle East accounting for the bulk of the capacity expansion. Growth in the BOPP film market is driven by rising demand from Asia, particularly from China and India, and other developing regions such as Latin America and Eastern Europe. Amongst the BOPP film market, stretch film machinery segment continues to witness exceptional growth. Cast film continues to make inroads into those application areas that are historically led by BOPP film. Significant advancements in process capabilities coupled with enhanced resins and improved equipment have filled most of the wide existing gap between BOPP film and Cast PP film.

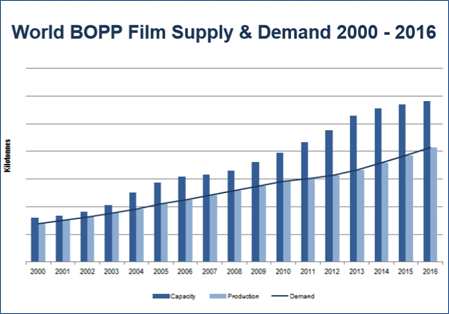

Demand for packaged foods, and the subsequent need for BOPP film packaging, has weathered the recession relatively well, facilitating world BOPP film demand growth of an average 6.1% pa over the last five years, to reach over 6 3 mln tons in 2011. PCI’s ‘conservative’ forecasts show world demand for BOPP films will continue to grow by an average of 6.6% per annum to reach 8.3 3 mln tons by 2016. Growth in Asian demand is expected to account for a vast majority of the predicted world growth over the next five years. Report highlights include:

* BOPP film producers have more than kept pace with demand growth and increased by 40% the size of production capacity since 2006. After a very busy year for sales of extrusion lines in 2010, decisions on new investment decisions have been delayed due to the state of the market.

* The Central and East Asian region (China, Japan, South Korea and Taiwan) is the world’s largest producer and consumer of BOPP films accounting for over half of global demand and capacity in 2011.

* Average world BOPP film ‘nameplate’ capacity utilisation during 2011 was around just 70% with Chinese producers having a tough time building a profitable business and have many of the new lines installed in China in recent years have been running slow or not at all during 2011.

* Flexible packaging applications for BOPP film now account for 80% of world demand.

* Capacity additions announced and expected, will expand the world BOPP film industry by another third over the industry size in 2011, with China again leading industry investment.

* The global BOPP film industry has seen a degree of consolidation in the last two years with Taghleef Industries emerging as the global leader.

* China is beginning to pose a threat in export markets, whilst planned capacity increases in India and the Middle East will be targeted at exports in the future.

Add Comment